Examples

GARCH(1, 1)

GARCH (acronym for generalized autoregressive conditional heteroskedasticity) is a well-known time series model used to describe the conditional variance of the errors in time-varying fashion. In this example, we show how the GARCH(1, 1) is simply a particular case of GAS; more specifically, it is a Normal GAS(1, 1) model with inverse scaling.

Note that this equivalence is true only under no reparametrization – it is necessary to modify the default link!, unlink! and jacobian_link! methods to use IdentityLink for the Normal distribution.

The code for this example can be accessed here.

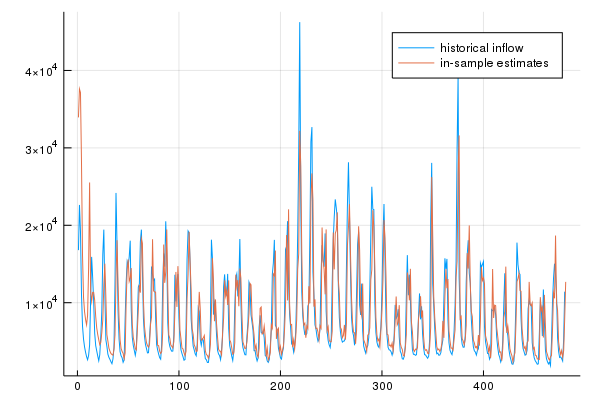

Water inflow

Let's model some monthly water inflow data from the Northeast of Brazil using a Lognormal GAS model. Since inflow is a highly seasonal phenomenon, we will utilize lags 1 and 12. The former aims to characterize the short-term evolution of the series, while the latter characterizes the seasonality. The full code is in the examples folder.

# Convert data to vector

y = Vector{Float64}(vec(inflow'))

# Specify model: here we use lag 1 for trend characterization and

# lag 12 for seasonality characterization

gas = Model([1, 12], [1, 12], LogNormal, 0.0)

# Estimate the model via MLE

fit!(gas, y)

# Obtain in-sample estimates for the inflow

y_gas = fitted_mean(gas, y, dynamic_initial_params(y, gas))

# Compare observations and in-sample estimates

plot(y)

plot!(y_gas)The result can be seen in the following plot.